What Happened in the Markets in June 2026

Geopolitical tensions and rising inflation drove June markets. Stocks finished mixed, but major indexes remained solidly positive for the first half of 2026.

Written by

Ryan Gubic

Published on

6

Jul 2026

Copy link

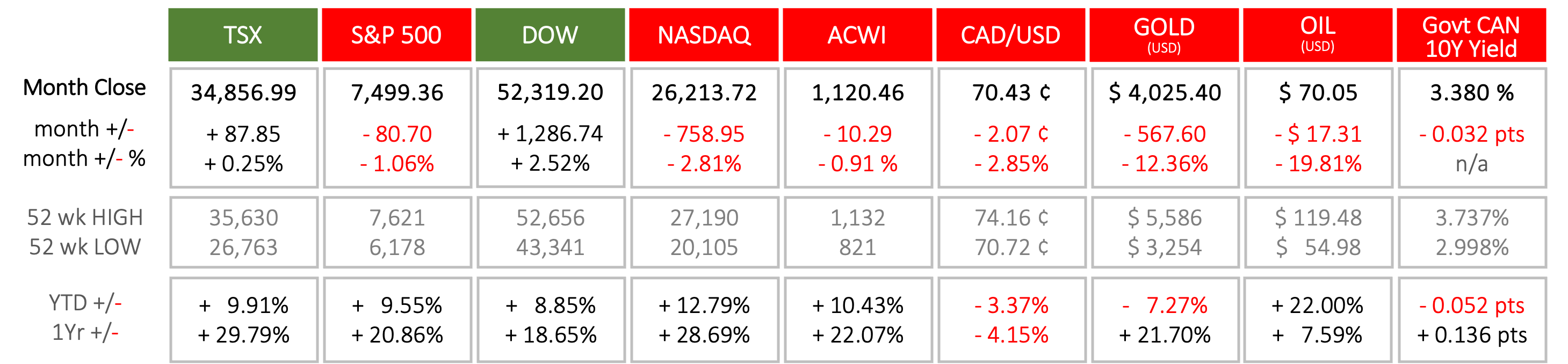

Last Month in the Markets: June 1st – 30th, 2026

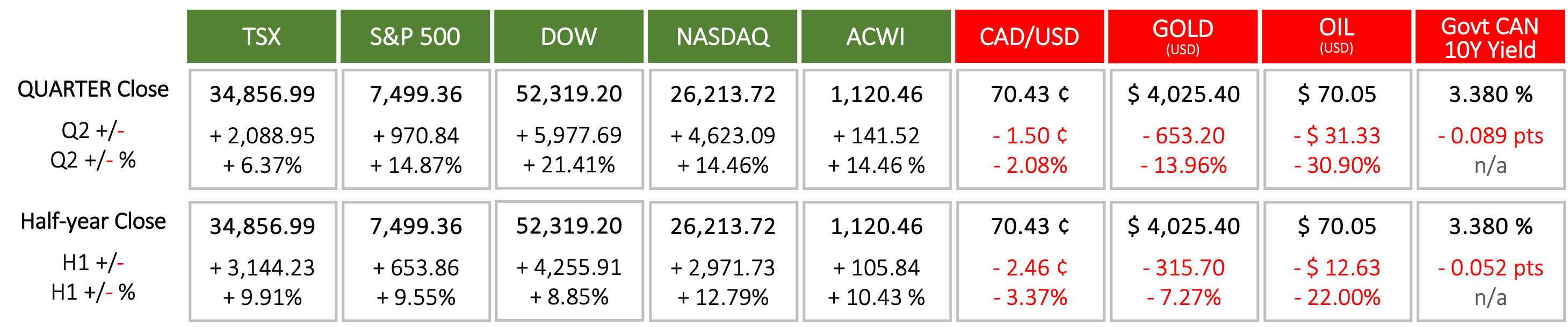

Last Quarter and First Half of 2026

Index returns based on index value (source: Bloomberg https://www.bloomberg.com/markets, MSCI https://www.msci.com/end-of-day-data-search and ARG Inc. analysis. Price returns are reflected)

What happened in June, this quarter and in the first half of this year?

The war in the Middle East, between the U.S. and Iran and between Israel and Gaza, Lebanon and other Arab countries and groups, continued to influence capital markets around the world. The closing of the Strait of Hormuz that carries a significant proportion of the world’s crude caused oil prices to spike in early April, in mid-May and again in early June. Since June 3rd, the price of oil has fallen 30% from its intraday high of $97. Oil ended June at the same price as the end of February.

In June, the performance of equities did not contribute to long term returns. The TSX almost broke-even, the S&P 500 lost 1%, the Dow rose 2½% and the NASDAQ lost about the same percentage as the Dow.

American equities experienced a tremendous quarter of performance. The TSX rose “only” 6%, while the S&P 500 and NASDAQ popped up 14% and the Dow jumped over 21%. Year-to-Date the TSX, S&P 500 and Dow have each risen 9%, and the NASDAQ, despite some days with major gains or losses, has grown 14%. For families seeking professional wealth management in Calgary, understanding what drives market returns, and how those developments impact your long-term financial plan, is where working with a trusted Personal CFO can make all the difference.

What’s ahead for July and beyond?

The renegotiation of CUSMA, NAFTA’s successor, is in jeopardy as the U.S. President has indicated reluctance and objection to a continental trade deal. On July 1st, the U.S. officially declined to renew the agreement that was created during Trump’s first term. Bilateral discussions continue between the countries, and negotiations are on-going to create side agreements among Canada, the U.S. and Mexico.

Progress, or its absence, on Middle East peace will affect markets for equities and commodities, and energy prices will heavily influence inflation. Rising inflation makes interest rate cuts unlikely, and although the price of crude has returned to pre-conflict levels, the high-priced oil has not passed through supply chains. Inflation is expected to continue to rise before it will lessen.

We all eagerly await the time when markets that are influenced by economic indicators like inflation, employment, rates, GDP and corporate performance, and the importance of geopolitical events fades.

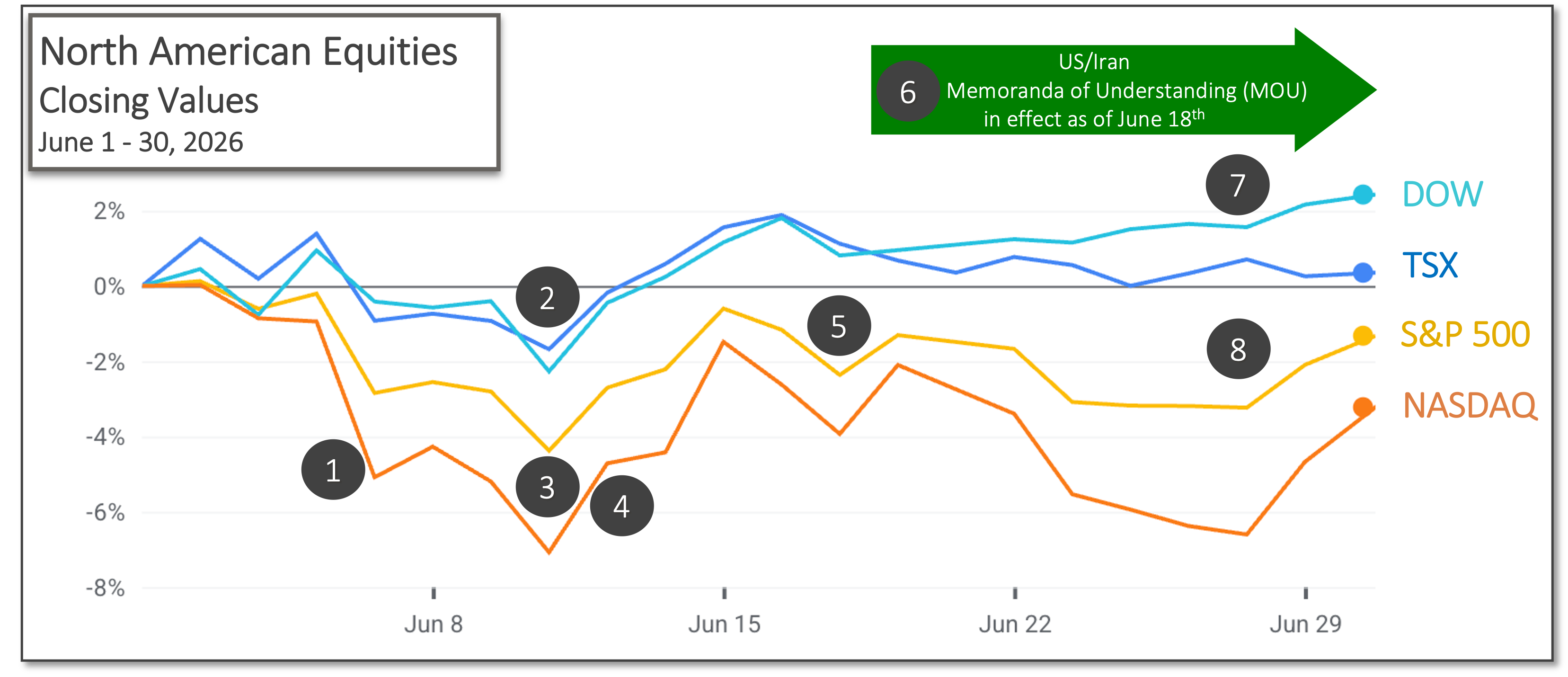

Events that influenced markets in June included:

(source: Bloomberg https://www.bloomberg.com/marketsand ARG Inc. analysis)

1. June 5th – Canadian and American employment growth rebounded

Canadian employment increased by 88,000 and the unemployment rate fell by 0.3 percentage points to 6.6%. This is the first significant gain since November 2025, and the number of full-time workers rose by 154,000 in May. CBC and LFS StatsCan's Labour Force Survey

According to the Bureau of Labor Statistics' Employment Situation Summary, total nonfarm payroll employment increased by 172,000 and the unemployment rate was unchanged at 4.3 percent. Job gains occurred in leisure and hospitality, local government and health care, while employment in financial activities declined.

Typically, increasing employment levels would be good news for equities, but the rising jobs and inflation rate (both foreign and domestic) could drive a corresponding rise in interest rates. The likelihood of a rate cut fell, and the changes of a rate increase this year rose. CNBC and jobs and rates

2. June 10th – Bank of Canada held rates steady, again

The Bank of Canada held its policy interest rate unchanged at 2.25%. Employment growth has been uneven, and inflation has risen in response to the increased price of energy since the conflict in the Middle East was reignited. Additionally, tariffs and the renegotiation of CUSMA will factor into the Bank’s next calculations and projections for interest rates. BoC release CBC and BoC

3. June 10th – U.S. inflation continued to rise

U.S. consumer inflation continued to accelerate. The Consumer Price Index (CPI) increased 0.5 percent on a seasonally adjusted basis in May, after rising 0.6 percent in April according to a release by the Bureau of Labor Statistics. Over the last 12 months, the all-items index increased 4.2 percent in May, up from 2.8 percent in April. The index for energy rose 3.9 percent in May and accounted for over sixty percent of the monthly all-items increase. CNBC and CPI

The U.S. Producer Price Index is also accelerating on a year-over-year basis. In May the annualized rate was 6.5 percent, which is the largest year-over-year rise since November 2022. BLS and PPI

4. June 11th – European Central Bank moved their rates higher

In response to rising inflation in the Eurozone, the European Central Bank raised its three benchmark rates by 0.25 percentage points. Their goal to provide consumer price stability at 2% inflation in the medium term is aligned with the goals of most central banks. ECB rate hike

5. June 17th – Federal Reserve’s policy interest rate remained unchanged

Newly installed Fed Chair, Kevin Warsh, announced that the policy interest rate, the federal funds rate, would be maintained in the range of 3½ to 3¾ percent. It was Warsh’s first interest-rate decision and press conference. An update to the Fed’s Summary of Economic Projections (SEP) was also released. Fed announcement

The SEP included with the interest rate decision predicted an increase for inflation, and removed the anticipated rate cut this year from the “dot plot”. The “hold” for rates was widely expected, but the SEP provided new information on the potential trajectory of American rates, which have an influence on other central banks and global economic growth.

Half of the committee members of the FOMC that sets interest rates now predict a rate hike, while the other half predict no change or a rate cut. The equal strength of these two opinions within the committee suggests that higher rates could be coming toward the end of the year according to CME's FedWatch tool.

6. June 18th – U.S./Iran Memoranda of Understanding (MOU) came into effect

After three days of heightened negotiations between the two countries, the U.S. and Iran agreed to a MOU to end hostilities over the next 60 days. BBC and MOU

7. June 22nd – Inflation breached 3 percent

Canada’s CPI rose 3.2 percent since last May, an increase from the year-over-year rate in April of 2.8%. May’s inflation rate was the highest since late 2023. The price of gasoline rose over 33% in May, which drove much of the consumer inflation reading. StatsCan CPI release CBC and CPI

8. June 25th – Canadian employment and wages continued to rise

Canadian payroll employment increased by 22,000 in April. On a year-over-year basis, employment has increased by 78,100. Job vacancies continued to hover around 500,000. Average weekly earnings were up 1.0% to $1,346 in April, and up 3.8% compared to April 2025. StatsCan release

9. June 25th – U.S. inflation breached 4% in May and import prices jumped

The Federal Reserve’s preferred inflation indicator, the Personal Consumption Expenditures Price Index (PCE) measured inflation at 0.4% in May and 4.1% on a year-over-year basis. Core PCE, which does not include more volatile food or energy, has risen 3.4% over the last year. PCE release CNBC and PCE

The price of U.S. imports rose 1.9% in May after rising 2.0% in April and 0.9% in March. Compared to May 2025, import prices have risen 6.7%, the largest increase since August 2022, when prices rose 7.7%. The cost of imported fuel rose 12.5% in May and has risen 47.0% since February. IPI release

Ryan Gubic is the founder of MRG Wealth Management Inc. operating as MRG Wealth (“MRG”) and is a Portfolio Manager with MRG investments of Aligned Capital Partners Inc. (“ACPI”). The opinions expressed are not necessarily those of MRG, ACPI, or Ryan Gubic. This material is provided for general information and the opinions expressed and information provided herein are subject to change without notice. Every effort has been made to compile this material from reliable sources however no warranty can be made as to its accuracy or completeness. Before acting on the information presented, seek professional financial advice based on your personal circumstances. ACPI is a full-service investment dealer and a member of the Canadian Investor Protection Fund (“CIPF”) and the Canadian Investment Regulatory Organization (“CIRO”). Investment services are provided through MRG Investments, an approved trade name of ACPI. Only investment-related products and services are offered through MRG Investments of ACPI and covered by the CIPF. Financial planning and insurance services are provided through MRG. MRG is an independent company separate and distinct from MRG Investments of ACPI.

Dollars and Sense

Discover more

Dive into some advice directly from our Founder and Personal CFO.

What Happened in the Markets in May 2026