Monthly Market Update - August 2025

TSX outperformed major indexes in August despite U.S. tariffs. Trade disputes, inflation, jobs data, and rate cut expectations shaped markets; uncertainty remains into fall.

Written by

Ryan Gubic

Published on

3

Sep 2025

Copy link

Last Month in the Markets: August 1st – 29th, 2025

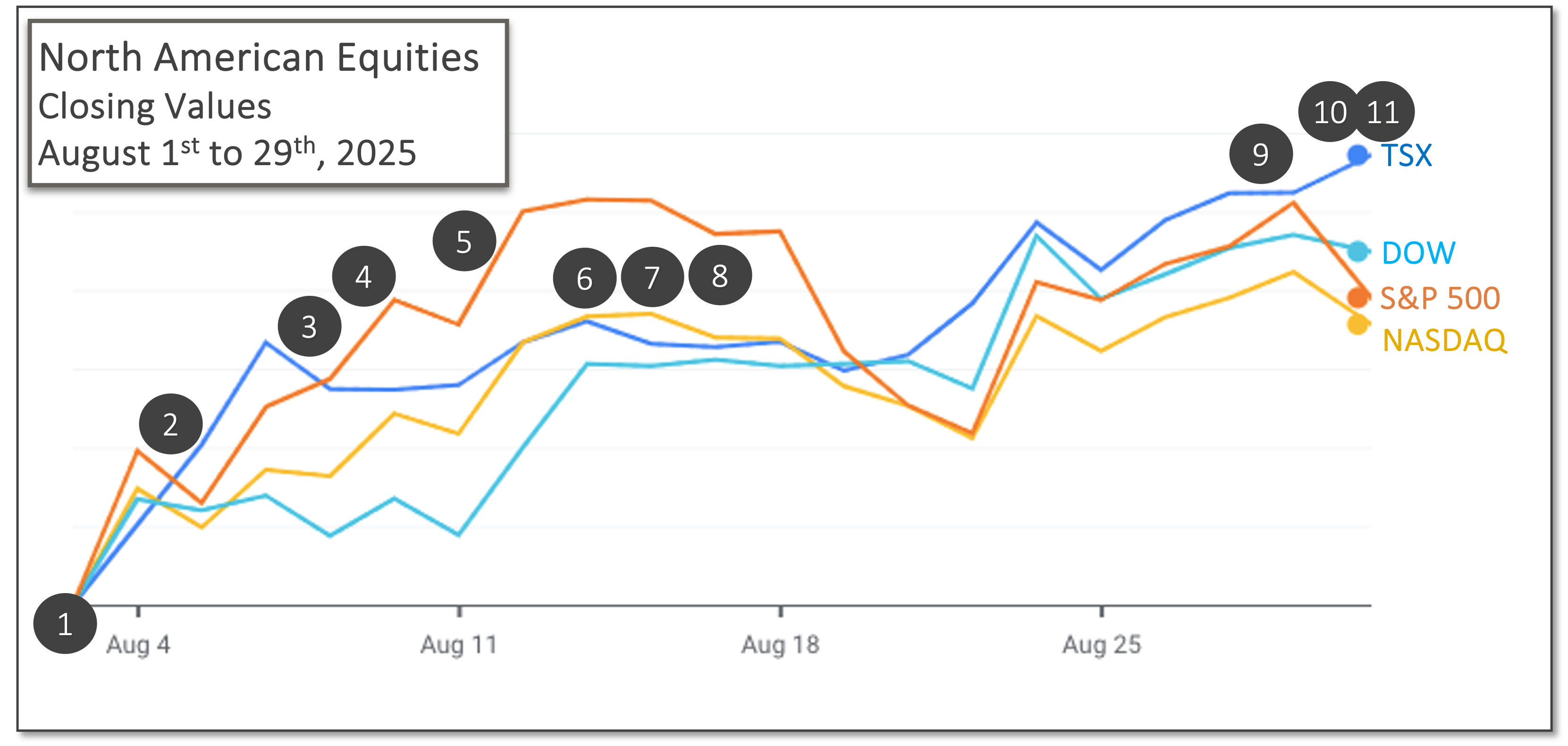

Index returns based on index value (source: Bloomberg https://www.bloomberg.com/markets, MSCI https://www.msci.com/end-of-day-data-search and ARG Inc. analysis)

What happened in August?

The TSX was the clear star among North American equity indexes last month moving nearly 5% above its closing value at the end of July. Not only did it best the S&P 500, Dow and NASDAQ in August, it leads all of them in year-to-date and one-year performance. This has occurred despite the threats and imposition of tariffs from the U.S. president and his administration, and the recently muted response from the Canadian government. Discuss your wealth management strategy with your financial advisor in Calgary to understand the impacts to your financial plan.

Economic reports and geopolitics that influenced markets in July included:

1. August 1st – Trump’s tariffs arrived

To begin the month, 35% tariffs were imposed on Canadian imports to the U.S. as negotiations continue. Talks or communication was not on-going at the highest level between Prime Minister Carney and President Trump when the tariffs came into force. Prime Minister Carney has indicated that negotiations with the U.S. president will resume when appropriate. CBC and Tariffs

The month began with a disappointing Employment Situation Summary that caused President Trump to fire the chief statistician at the Bureau of Labor Statistics. Trump has been calling for an interest rate reduction, and the economy’s poor job performance could trigger a rate drop.

2. August 5th – trade deficits affected by threatened and enacted tariffs

Canada’s trade deficit continued to widen and reached its second highest monthly level at $5.9 Billion. Imports grew faster than exports as inbound shipments of high value oil equipment arrived in June. Exports to the U.S. have fallen to 70% of total exports, compared with 83% in June 2024. Reuters and Can trade balance

The Bureau of Economic Analysis announced that June’s U.S. trade deficit shrank 16% to $60.2 Billion as exports eased 0.5% (-$1.3 Billion) and imports fell 3.7% (-12.8 Billion) compared to May. The trade deficit reached its lowest level in two years as the trade gap with China and imports of consumer goods dropped sharply. BEA release Reuters and US trade balance

3. August 7th – China’s exports surged to skirt U.S. tariffs

China’s exports increased more than expected in July. Shipments sent to other countries that often forward Chinese goods on to the U.S. jumped. Shipments directly to the U.S. fell more than 20%. Overall, China’s exports grew by 7.2% compared with July 2024. NYT and China's trade

4. August 8th – Canadian employment fell dramatically, U.S. CPI rose

Canadian employment declined by 41,000 jobs in July according to StatsCan’s Labour Force Survey after an increase of 83,000 in June. The employment rate fell 0.2% to 60.7% and the unemployment rate was unchanged at 6.9%. Analysts expected employment to increase by 13,500 and unemployment to tick up to 7.0%. The employment decline was concentrated among youth aged 15 to 24 (-34,000). The industries that lost the most jobs was information, culture and recreation (-29,000) and construction (-22,000). CBC and Labour Force Survey

5. August 11th – China’s tariffs given 90-day reprieve

President Trump signed a 90-day extension delaying the introduction of 145% tariffs on Chinese imports, and China delayed its retaliatory tariffs of 125% on U.S. imports. The existing tariffs on imports from and exports to China are 30% and 10%, respectively. CNBC and China tariffs

6. August 12th – U.S. inflation may not delay Fed rate cuts

The CPI increased 0.2% for the month and 2.7% on a year-over-year basis. Core CPI, which excludes more volatile food and energy price changes, increased 0.3% for the month and 3.1% compared to last year. Core inflation rose more rapidly in July than it has in the past five months. With delays and renegotiations, July prices do not yet reflect all the effects of threatened and implemented tariff, suggesting that inflation could continue to increase in the coming months. CNBC and CPI BLS CPI release NYTimes and CPI

Many analysts believe the weakness in the employment situation will encourage the Federal Reserve to cut interest rates despite rising inflation in July. On the morning of the CPI announcement CME's FedWatch tool listed the probability of a rate cut on September 17th at 94%.

7. August 14th – Producer inflation soared

The Bureau of Labor Statistics released the Producer Price Index (PPI) showing that wholesale prices jumped 0.9% in July, after holding steady in June and rising 0.4% in May. The year-over-year rate of producer inflation grew to 3.3% for July, the highest rate in 5 months when February’s PPI was 3.4%. BLS PPI release

8. August 15th - Trump and Putin met in Alaska

U.S. President Donald Trump met with Russian leader Vladimir Putin in Alaska to discuss his war with Ukraine. President of Ukraine, Volodymyr Zelenskyy, was not invited to the summit meeting, whose exclusion drew the ire of NATO and the European Union leaders. The progress, if any, achieved from the summit has not materialized in a meaningful manner, yet. CBC and Alaska Summit

9. August 28th – U.S. Gross Domestic Product revised upward

During the period of April through June the U.S. economy grew by 3.3%, better than the 3.0 estimated initially. Imports subtract from GDP total in the calculation, and after stockpiling before tariffs were introduced, imports in the latter stages of the quarter fell by nearly 30%, which propped up GDP numbers. CNBC and GDP

10. August 29th – Canadian economy shrank

StatsCan reported that Gross Domestic Product declined by 0.4% in the second quarter after rising 0.5% in the first quarter. The decline was driven by substantial reductions in exports (down 7.5% in Q2) and business investments in machinery and equipment. U.S. initiated tariffs and Canada’s response, and the underlying uncertainty caused by the trade conflict, created the environment for an economic slowdown. StatsCan release

11. August 29th – PCE inflation remained above goal, tariffs deemed illegal, and rates could fall

The Federal Reserve’s preferred inflation indicator, the Personal Consumption Expenditures (PCE) price index rose 2.6% over the past year, and core inflation that excludes food and gasoline rose 2.9%. Both are above the Fed’s goal of 2% showing tariffs imposed by Donald Trump have raised prices. Inflation has returned to February’s level, which had been falling until tariffs were announced. BEA PCE release CNBC and PCE

A federal appeals courts has declared that Trump’s tariffs are illegal after upholding a May ruling by the Court of International Trade. The tariffs will remain in-place temporarily to allow a further appeal to the U.S. Supreme Court. BBC and tariff ruling

Also, despite the mixed economic news CME's FedWatch tool has increased the likelihood of a cut to the federal funds rate by the Federal Reserve on September 17th.

What’s ahead for September and beyond?

Important news will arrive on September 17th when the Bank of Canada and the U.S. Federal Reserve announce their interest rate decisions. Canadian inflation is in-range of the 2% goal, and jobs growth has ended. The prediction as of Labour Day has the likelihood of a Fed rate cut at about 90%, as U.S. inflation is above goal, which could delay rate cuts, but jobs growth is slowing, which encourages a rate cut.

The imposition of tariffs and retaliatory trade manoeuvres suggest that inflation will continue to rise, and jobs growth will continue to fall. With a potential Supreme Court ruling on the legality of President Trump’s tariffs in October, uncertainty will continue until at least the autumn, if not longer.

Trade and tariff negotiations between Canadian and American leaders continue in the shadow of a looming Supreme Court appeal, and the scheduled CUSMA review in July 2026. CBC and CUSMA review

The trade and interest rate situation will heavily influence market performance for some time.

Ryan Gubic is the founder of MRG Wealth Management Inc. operating as MRG Wealth (“MRG”) and is a Portfolio Manager with MRG investments of Aligned Capital Partners Inc. (“ACPI”). The opinions expressed are not necessarily those of MRG, ACPI, or Ryan Gubic. This material is provided for general information and the opinions expressed and information provided herein are subject to change without notice. Every effort has been made to compile this material from reliable sources however no warranty can be made as to its accuracy or completeness. Before acting on the information presented, seek professional financial advice based on your personal circumstances. ACPI is a full-service investment dealer and a member of the Canadian Investor Protection Fund (“CIPF”) and the Canadian Investment Regulatory Organization (“CIRO”). Investment services are provided through MRG Investments, an approved trade name of ACPI. Only investment-related products and services are offered through MRG Investments of ACPI and covered by the CIPF. Financial planning and insurance services are provided through MRG. MRG is an independent company separate and distinct from MRG Investments of ACPI.

Dollars and Sense

Discover more

Dive into some advice directly from our Founder and Personal CFO.

What Happened in the Markets in June 2026