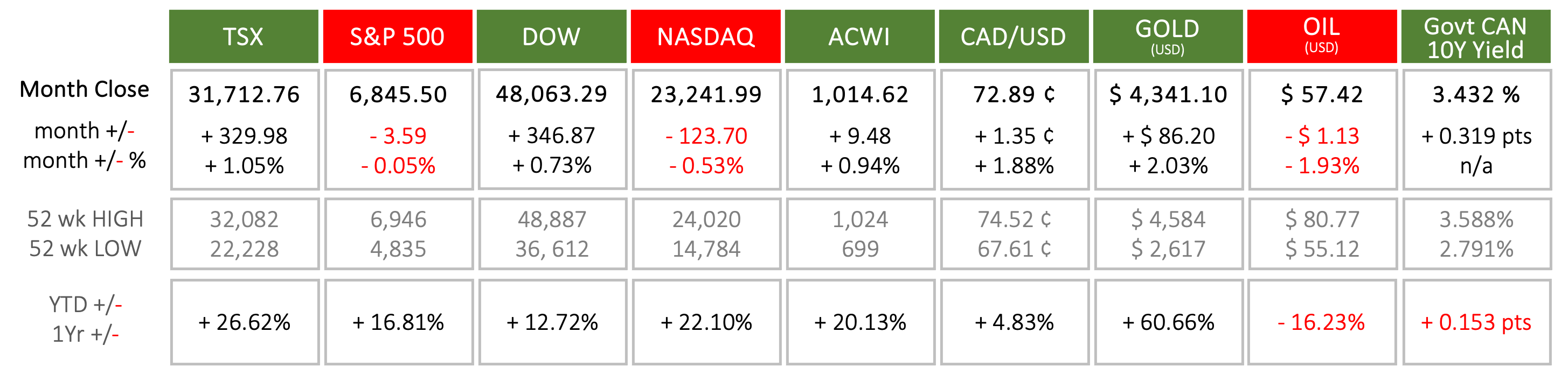

Annual Markets Review - 2025

Markets rose strongly overall despite an April tariff shock that sparked a brief global selloff; volatility peaked then eased, stocks hit new highs, gold surged, and oil fell.

Written by

Ryan Gubic

Published on

13

Jan 2026

Copy link

Last Month in the Markets: December 1st – 31st, 2025

Last Year in the Markets: January 2nd - December 31st, 2025

(source: Bloomberg https://www.bloomberg.com/markets, MSCI https://www.msci.com/end-of-day-data-search and ARG Inc. analysis)

What happened in 2025?

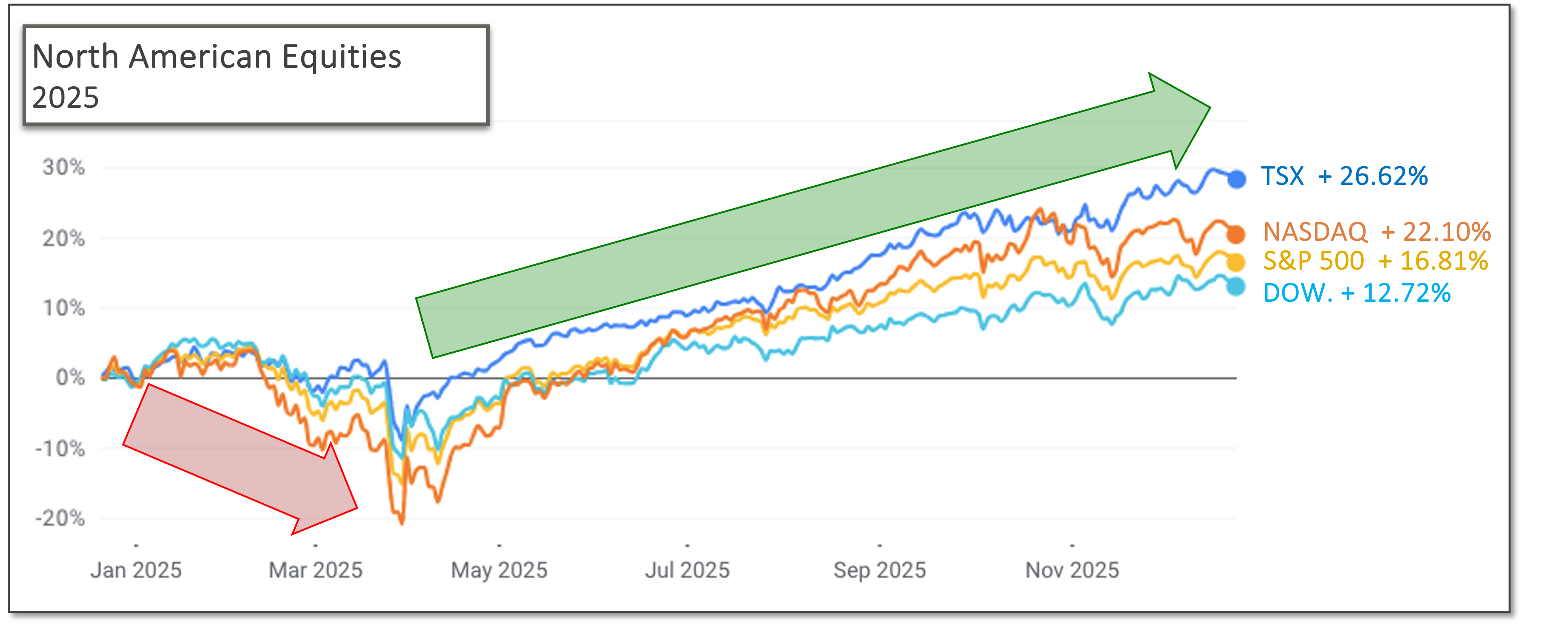

Last year was productive, again, for equity investors, with Canadian and American indexes delivering remarkable returns for the third consecutive year. It was not clear-sailing for the entire year. The first quarter limped along until President Trump conducted an Independence Day ceremony from the White House Rose Garden on April 2nd. Instead of the traditional celebration on July 4th with red-white-and-blue bunting and parades, he introduced a sweeping array of tariffs that ignited a global trade war.

By Friday, April 4th, the North American equity indexes had plunged between 6.32% and 10.02% for the week. The All Country World Index lost 7.91% over the same period, signifying the depth and breadth of the negative effects of tariffs on equity values around the world. Fortunately, by mid-May the TSX, S&P 500, Dow and NASDAQ had erased the losses of the first week of April.

(source: Bloomberg https://www.bloomberg.com/marketsand ARG Inc. analysis)

Delays in implementing the tariffs on U.S. imports allowed markets to calm, and negative financial effects were postponed. When other nations, particularly China, promised retaliatory tariffs on U.S. exports, or when nations increased American access to their markets, or foreign leaders delivered gifts to the President previously announced tariffs were cancelled, reduced or delayed.

The VIX Index that measures volatility and signals fear and stress sin the market peaked on April 4th. Twice the VIX has peaked higher, In October 2008 during the world financial crisis and March 2020 at the onset of the global pandemic. Equities and the VIX are inversely corelated, meaning that they usually move in opposite directions. Thankfully, the VIX has returned to levels that signify more stability. From the VIX’s peak and equities’ trough in early April they have moved in opposite directions with equity indexes setting all-time highs late in 2025.

The geopolitical uncertainty that underscored Trump’s trade war drove some investors to the safe haven of gold, and its price to an all-time high and a gain in value of more than 60% in 2025. Perceived and actual declines in global growth reduced the demand, and therefore the price, for oil. The price fell more than 16% last year and closed below $58.

What’s ahead in 2026?

The uncertainty and volatility seen in 2025 will likely continue, but it is difficult to imagine that a single event on a single day, like Trump’s tariff announcements in early April, could be repeated with the same immediate and lingering effects. Regardless of your political stance, interpreting political and economic events through the lens of your financial goals when making investment decisions remains the purpose of investment management.

As always, monetary policy will heavily influence capital markets and will be based on inflation and employment data and trends. Additional intrigue will follow as Fed Chair, Jerome Powell, is under investigation for misleading congress. It does not appear that he will allow himself to be subjected to partisan political threats based on his response to news of the emerging case against him.

The end of January, when the Canadian and American central banks will make rate decisions on the same day, will begin 2026 in earnest. The Bank of Canada and Federal Reserve will both announce interest rate decisions on January 28th, March 18th, April 29th, October 28th and December 9th. On June 10th, July 15th and September 2nd the Bank of Canada will announce, which is one or two weeks ahead of the Fed’s scheduled rate-dates.

As each announcement date approaches, markets will price-in the anticipated monetary policy move. A surprise decision would likely lead to volatility in equity markets, and predicted manoeuvres will not create rapid and unexpected value adjustments.

Global and domestic Gross Domestic Product measuring economic output will move the price of oil, and geopolitical uncertainty will push the price of gold. These generally accepted principles and relationships will have exceptions, yet they are predictable based on their history. It appears that unpredictability will begin with the actions and decisions of the U.S. Supreme Court, legislative bodies and president.

Since investing solely in GICs will not deliver risk-free after tax returns that beat inflation, none of us will be immune to uncertainty. Managing risk consistent with your individual situation, while maximizing returns within this constraint, remains the paramount consideration for investment decisions, goal-setting and financial planning. If you have questions, schedule an introduction call and discover the wealth management Calgary families trust to have clarity, confidence, and freedom in their lives.

Summary of economic events that contributed to market performance in 2025:

1. January 10th – Employment rose dramatically to close 2024

StatsCan’s Labour Force Survey reported that Canadian employment rose by 91,000 in December. The unemployment rate declined slightly by 0.1 percentage points to 6.7%. The increase to was almost four times the amount anticipated by analysts and economists. StatsCan release CBC and LFS

U.S. employment increased by 256,000 in December, which was 38% above the 2024 monthly average of 186,000. The unemployment rate remained constant at 4.1%, and the number of unemployed people did not change in December and sits at 6.9 million. BLS release

2. January 15th – U.S. CPI rose on energy prices

Consumer prices rose 0.4 percent in December, and the all-items index increased by 2.9 percent over the last year according to the U.S. Bureau of Labor Statistics. Over 40 percent of the month’s increase is attributed to energy prices. BLS CPI release CNBC and December 2024 CPI

3. January 17th - China’s economy grew rapidly in Q4

China’s economy expanded 5.4% in the in fourth quarter, exceeding expectations. Full year GDP growth reached 5% as stimulus measures delivered results. CNBC and China GDP

4. January 20th – Trump became President, again

Donald Trump was inaugurated as the 47th President of the United States in a ceremony on the Rotunda of the Capital Building. Within the first days of his presidency over one hundred executive orders were signed to further his agenda.

5. January 24th – Trump wasted no time in threatening tariffs

As of his first Friday after returning to office, Trump’s threatened tariffs had not materialized. A February 1 implementation date for 25% tariffs against Canada and Mexico imports has been repeatedly mentioned. In some statements tariffs are designed to facilitate the tightening of borders that permit drugs and illegal immigrants to enter the U.S.

President Trump has suggested that firms could relocate production to the U.S. to avoid paying tariffs, and that tariffs would generate revenue for the U.S. government. CNN and tariffs CBC and tariffs The Guardian and tariffs Global and threats

6. January 29th – BoC cut rates to start the year

The Bank of Canada lowered its policy interest rate by 25 basis points, the U.S. Federal Reserve held rates steady and the European Central Bank took the same decision as Canada.

7. January 31st – U.S. inflation remained above target

The U.S. Bureau of Economic Analysis released the Personal Consumption and Expenditures (PCE) price index, the Federal Reserve’s preferred inflation indicator. On a monthly basis headline PCE rose 0.3% and 2.6% on a year-over-year basis for December. Both figures were aligned with expectations and are above the Fed’s targets. CNBC and PCE BEA release

8. February 7th – Employment growth high in Canada, slowed in U.S.

StatsCan’s Labour Force Survey reported that employment increased by 76,000, which triple the expectation of analysts. The unemployment rate fell by 0.1% to 6.6%. Wages for permanent employees have risen 3.7% on a year-over-year basis. Wage rate growth is closely watched by the Bank of Canada as a leading inflation indicator. StatsCan release CBC and LFS

The U.S. Bureau of Labor Statistics released its Employment Situation Summary showing that nonfarm payroll rose by 143,000 in January. Unlike Canada, this is below the expectation of 169,000 and significantly less than December’s 307,000. The unemployment rate in January lowered slightly to 4.0%. The market has interpreted the less-than-stellar report as not weak enough to push the Federal Reserve back into rate cutting mode. CNBC and jobs

9. February 12th – U.S. inflation higher than expected

After rising 0.4 percent in December, the Consumer Price Index (CPI) increased 0.5 percent in January. Over the past 12 months the all-items index increased 3.0 percent before seasonal adjustment. About 30 percent of the month’s increase was attributed to the index for shelter. The energy index increased 1.1 percent, and gasoline rose 1.8 percent in January adding to rising inflation. Equity values moved downward after the Bureau of Labor Statistics release. Rising prices suggest that the Federal Reserve will delay interest rate reductions until the second half of 2025. CNBC and January CPI

10. February 21st – Fed minutes indicated inflation expectations

The Federal Reserve released the minutes from its January 28-29th meeting that held interest rates steady. The committee noted that businesses would attempt to pass input cost increases to consumers arising from tariffs, and that inflation expectations had increased recently. The expectation for rising inflation continues to push the next Fed rate reduction further into the future, likely in the summer or autumn. A delay in rate cuts by the Fed placed additional negative pressure on stock values. CME FedWatch tool FOMC minutes

11. February 28th – Canadian GDP rose slightly, U.S. corporate results soared, PCE moderated

Canadian Gross Domestic Product (GDP) rose 0.2% in December after declining by the same proportion in November. Fourth quarter GDP increased 0.6% after rising 0.5% in the third quarter. Overall household spending rose 1.4% in the fourth quarter and 2.4% in 2024. December GDP Q4 GDP

The quarterly earnings season concluded for S&P 500 companies with an average earnings gain of 17.8% over the same period one year ago. It was the strongest growth since the fourth quarter of 2021. Financials posted an earnings gain of 56%, the highest of all 11 sectors. FactSet Earnings Insight

The U.S. Federal Reserve’s preferred inflation indicator, the Personal Consumption Expenditures price index (PCE) rose 2.5% in January and core PCE that excludes food and energy increased 2.6%. January’s performance was slight improvement from December’s levels. BEA PCE release

12. March 6th – ECB interest rates cut

The European Central Bank (ECB) cut its interest rates by ¼ percent (25 basis points), which set its interest rates on the deposit facility, the main refinancing operations and the marginal lending facility at 2.50%, 2.65% and 2.90%, respectively. ECB release

13. March 7th - Canada and the United States released employment data for February

In Canada, employment was virtually unchanged (+1,000) and the unemployment rate held steady at 6.6%. StatsCan release

According to the Bureau of Labor Statistics (BLS), U.S. jobs rose by 151,000 in February, which was higher than expected, while the unemployment rate was unchanged at 4.1%. Wages have risen 4.0% over the last year. The latest U.S., jobs data suggests that the next Federal Reserve rate cut will occur in the second half of 2025. BLS release CNBC and jobs CME FedWatch

14. March 12th – interest rates and inflation

The Bank of Canada reduced its target for the overnight rate again. The announcement included, “the pervasive uncertainty created by continuously changing US tariff threats is restraining consumers’ spending intentions and businesses’ plans to hire and invest. Against this background, and with inflation close to the 2% target, Governing Council decided to reduce the policy rate by a further 25 basis points to 2.75%.”

U.S. consumer prices increased 0.2 percent in February, and on a year-over-year basis the all-items index increased 2.8 percent before seasonal adjustment. In January, the monthly inflation increase was 0.5 percent, and the annualized inflation rate was 3.0 percent. BLS release

15. March 14th – New Prime Minister of Canada

On Friday, Mark Carney, former central banker, replaced Justin Trudeau as Prime Minister. Unrelated to this change, North American equity indexes rose for the second consecutive Friday.

16. March 19th – Federal Reserve interest rate announcement

The Federal Reserve kept U.S. interest rates steady. The statement included, “In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will consider a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.” The Fed is watching the effects of the Trump administration’s actions to imposes tariffs and trade restrictions, and the resulting responses from sovereign nations affected by the trade war. The Fed will continue to maximize employment and return inflation to its long-run target of 2 percent even as “uncertainty around the economic outlook has increased.”

17. March 28th – U.S. inflation rose, Canadian GDP grew, and leaders talked

Equities initially moved lower again with the U.S. Bureau of Economic Analysis' release of the Personal Consumption Expenditures price index (PCE), which is the Federal Reserve’s preferred inflation measure. Inflation for February was 2.5% and Core PCE, excluding food and energy, ticked higher than expected to 2.8% from one year ago. The uncertainty surrounding inflation and tariffs continues to linger and delay CME's FedWatch prediction of lower rates to June and July. CNBC and PCE

Canadian Gross Domestic Product (GDP) rose 0.4% in January, a slight increase over the 0.3% increase in December. 13 of 20 sectors rose with goods-producing sectors delivering the largest increase at 1.1% for the first month of 2025. Mining, quarrying, and oil and gas extraction provided the largest increase in January. The largest drag on growth occurred in the retail trade sector, which contracted 0.9%. Tariffs are affecting February growth, when GDP is estimated to be unchanged. StatsCan release CBC and GDP

18. April 2nd – Trump launched global trade war

At a mid-afternoon press conference from the White House Rose Garden, Donald Trump imposed tariffs on imports from 185 countries and territories. Watch CNBC

The calculation to determine the tariff rate is not an accepted practice used by economists and assumes that a trade deficit represents the sum of all unfair practices by the foreign counterpart. Trump stated that the calculation included currency manipulation and other barriers, but these factors are not included in the mathematical formula. A report from the Cato Institute, which is based on 2023 World Trade Organization data, calculates China’s trade-weighted average tariffs at 3%. Trump imposed a minimum tariff of 10% bypassing his own calculation, since it was applied on 115 countries that the U.S. has a trade surplus.

19. April 4th – Canadian employment dropped in March, rose in U.S.

Employment data was released in Canada and the U.S. for March. StatsCan determined Canadian employment fell by 33,000, the first decline since January 2022, the employment rate declined 0.2% and the unemployment rate rose 0.1% to 6.7%.

The total nonfarm payroll employment rose by 228,000 and the unemployment rate changed little according to the Employment Situation Summary from the U.S. Bureau of Labor Statistics. Job gains were made in health care, social assistance, transportation and warehousing, and retail trade. Federal government employment declined.

20. April 10th – U.S. inflation fell slightly

In more encouraging news, the U.S. Bureau of Labor Statistics announced that the Consumer Price Index (CPI) rose 2.4% in March on a year-over-year basis. The same measure one month ago was 2.8%. Core CPI that excludes more volatile food and energy was also 2.8%, which is its lowest level in four years. BLS release

21. April 15th – Canadian consumer inflation dipped lower

StatsCan announced that the Consumer Price Index (CPI) for March was 2.3% on a year-over-year basis, down from 2.6% in February. The slowdown in price increases was driven by lower prices for travel and gasoline in March. StatsCan CPI release CBC and CPI

22. April 16th – Bank of Canada held rates steady, and ECB dropped ¼ point

The Bank of Canada maintained its target for the overnight rate at 2.75% and released its Monetary Policy Report (MPR). Tiff Macklem, Bank of Canada Governor, indicated that the “dramatic protectionist shift in US trade policy and the chaotic delivery have increased uncertainty, roiled financial markets, diminished global growth prospects and raised inflation expectations” in his opening statement to announce the rate decision.

23. April 28th – Canada re-elected Liberals and Prime Minister Mark Carney

At the end of the five week campaign the Liberals won 169 seats, 3 short of number needed to obtain a majority government. The official opposition will be the Conservatives with 144 seats. Elections Canada results

24. April 30th – American and Canadian Gross Domestic Product (GDP) declined

Canadian real GDP was 0.2% lower in February, following a 0.4% increase in January. Goods producing industries fell 0.6%, services-producing industries slipped 0.1% in February. Mining, oil and gas extraction, construction, real estate, rental and leasing declined while durable goods, finance and insurance rose. StatsCan and GDP

American GDP decreased at an annual rate of 0.3 percent in the first quarter of 2025 according to the advance estimate released by the Bureau of Economic Analysis. In the fourth quarter of 2024, real GDP increased 2.4 percent. BEA release

25. May 2nd – U.S. economy contracted in Q1, and job growth remained strong in April

American GDP decreased at an annual rate of 0.3 percent in the first quarter of 2025 according to the advance estimate released by the Bureau of Economic Analysis. For reference, in the fourth quarter of 2024, real GDP increased 2.4 percent. BEA release

U.S. nonfarm payroll employment increased by 177,000 in April and the unemployment rate was unchanged at 4.2 percent according to the Bureau of Labor Statistics’ press release.

26. May 12th – Temporary truce between U.S. and China sent stocks soaring

U.S. tariffs on most Chinese goods have been reduced to 30 percent and China has reduced its tariffs on most U.S. goods to 10 percent. The size of the cuts to the proposed tariffs, on both sides, and the speed of the agreement contributed to the size of the surprise and the size of the increase for equity indexes. New deal for US and China

27. May 13th and 14th – Positive inflation news contributed to equities rally

According to the Bureau of Labor Statistics, over the last 12 months, the all-items Consumer Price Index (CPI) increased 2.3 percent before seasonal adjustment. BLS CPI release

U.S. Producer Price Index fell 0.5 percent in April after being unchanged in March and increasing 0.2 percent in February. On an unadjusted basis, the index for final demand rose 2.4 percent for the 12 months ended in April. BLS PPI release

28. May 16th – Moody’s downgraded U.S. government credit rating

The U.S. government had its creditworthiness rating downgraded by Moody’s, which followed the same conclusion reached previously by S&P Global ratings in 2011 and Fitch Ratings in 2023. Moody’s had held a perfect rating for the U.S. since 1917. The rating of the government’s ability to repay its debts is no longer at the highest level for all of the major ratings agencies. BBC and Moody's

29. May 20th – Canadian inflation slowed below Bank of Canada target

The Canadian Consumer Price Index (CPI) rose 1.7% year-over-year in April, down from a 2.3% increase in March. The lower inflation rate was led by energy prices that fell by 12.7% in April, after a 0.3% decline in March. However, inflation for food purchased in stores increased to 3.8% in April, following a 3.2% increase in March. The Bank of Canada attempts to limit the long-run average inflation rate to 2%. StatsCan and CPI

30. May 21st – Legislative progress drove markets downward

The U.S. House of Representatives passed a “big, beautiful bill” that the non-partisan Congressional Budget Office predicts will increase the federal deficit by $3.8 Trillion over the next decade. On Wednesday, after the House narrowly passed bill that brings multitrillion dollar tax and spending cuts, U.S. equity markets fell. CNBC and budget bill

The increasing deficit coupled with higher interest rates linked to the lower credit rating will bring higher borrowing costs and, ultimately, contribute further to the federal deficit. CNBC and big bill

31. May 23rd – Canadian retail sales continued to increase

Retail sales increased for the fourth consecutive quarter as six of nine subsectors saw increases. The largest increases were seen at motor vehicle and parts dealers, while sales at gasoline stations and fuel vendors fell in response to lower prices. StatsCan and retail sales

32. May 26th – Tariff delay for EU moved markets higher

Equities jumped after President Trump announced two days after its introduction that a new 50% tariff on European Union imports would be delayed until July 9th. EU tariffs delayed

Expect more uncertainty based on a new 50% U.S. tariff on steel and tit-for-tat countermeasures. Steel tariffs of 50% and EU

33. May 27th – King Charles delivered throne speech to Parliament

King Charles delivered the speech from the throne to open Parliament for the newly elected Liberal government under Prime Minister Mark Carney. The priorities to eliminate interprovincial trade barriers, develop diverse international trading partners, deliver a middle class tax cut, increase housing, reduce tax on new homes, and manage immigration were reiterated. Throne speech

34. May 28th and 29th – Uncertainty over U.S. tariffs continued

The U.S. Court of International Trade (USCIT) ruled that Trump did not have the authority to impose the program of tariffs, which sent stocks upward. After a prompt appeal by the administration, a federal appeals court placed a temporary hold on the USCIT ruling. Stocks declined in response to the continuation of restrictive trade tactics. NBC News and rulings

35. May 29th and 30th – Canadian employment fell while GDP maintained its pace

Canadian payroll employment decreased by 54,000 in March following a decline of 40,200 in February. On a year-over-year basis, payroll employment was up 32,800 despite the last two months of decline. StatsCan and employment

Canadian GDP increased 0.5% in the first quarter of 2025, the same pace as the fourth quarter of 2024. Increased exports of passenger vehicles (+16.7%), industrial machinery, equipment and parts (+12.0%) were driven by the looming threat of U.S. tariffs. StatsCan Q1 GDP

36. June 4th – Bank of Canada maintained interest rates

The Bank of Canada (BoC) held interest rates unchanged for the second consecutive decision. The policy interest rate, the Canadian overnight rate, was kept at 2.75%. The BoC announcement included, “With uncertainty about US tariffs still high, the Canadian economy softer but not sharply weaker, and some unexpected firmness in recent inflation data, Governing Council decided to hold the policy rate.” CBC, tariffs and rates

37. June 5th – European Central Bank lowered rates

In contrast to the BoC, the European Central Bank lowered its interest rates by ¼ percent as inflation hovers around the Governing Council’s 2% medium-term target. ECB rate announcement

38. June 6th – Jobs reports from U.S. and Canada showed employment waning

The Bureau of Labor Statistics reported its Employment Situation Summary, showing nonfarm payroll employment increased by 139,000 in May, and the unemployment rate was unchanged at 4.2 percent. The average monthly gain over the last 12 months has been 149,000, slightly more than the U.S. job growth in May. BLS release

StatsCan announced that employment was little changed in May (+8,800). The employment rate held steady at 60.8 percent, and the unemployment rate rose 0.1 percentage points to 7.0 percent. From October 2024 to January 2025 Canadian employment increased by 211,000, but there has been virtually no additional employment in the last four months. StatsCan release

39. June 12th – Rising tensions in the Middle East affected market performance

Israel’s attack on Iran’s nuclear installations and military leadership, and Iran’s predictable response caused stocks, oil and gold to react. Stocks were down sharply the next day, except for energy stocks as oil jumped, as did gold.

40. June 18th – Federal Reserve continued its wait-and-see approach

The U.S. Federal Reserve chose to maintain interest rates at their current levels. The statement included, “The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook has diminished but remains elevated. The Committee is attentive to the risks to both sides of its dual mandate. In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4¼ to 4½ percent.” Fed announcement and press conference

41. June 22nd – U.S. bombed Iran

Over the weekend, as tensions continued to rise, President Trump executed a three-site bombing raid on Iran. The destruction of Iran’s nuclear capabilities was the goal. Oil prices have risen about 10 percent recently due to the conflict with Iran. A reduction in Iran’s oil exports or production in the Middle East caused by U.S. actions will harm China directly, and further strain relations with the U.S. NYT and US raid

Two days later President Trump announced a ceasefire between Israel and Iran.

42. June 24th – Canadian inflation stayed below Bank of Canada goal

The Consumer Price Index (CPI) rose 1.7 percent on a year-over-year basis in May, matching April’s rate. On a monthly basis, the CPI rose 0.6 percent in May. A smaller price increase for rent and a decline in travel tours put downward pressure on the CPI in May. Excluding energy, the CPI rose 2.7 percent in May, compared with 2.9 percent in April. StatsCan and CPI

43. June 26th and 27th – U.S. and Canadian Gross Domestic Product fell

American GDP decreased at an annual rate of 0.5 percent in the first quarter of 2025. In the fourth quarter of 2024, before President Trump started a global trade war, GDP increased 2.4 percent. BEA GDP release

Canadian GDP edged down 0.1 percent in April, following a 0.2 percent increase in March. Goods producing industries were down 0.6 percent in April, with the manufacturing sector accounting for nearly all the decline. Services-producing industries were up 0.1 percent in April. StatsCan and GDP

44. June 27th – U.S. inflation rose slightly above Federal Reserve’s goal

Personal income fell $109.6 Billion and disposable personal income decreased $125.0 Billion in May. The Personal Consumption Expenditures (PCE) price index, the Federal Reserve’s primary inflation indicator, for May increased 2.3 percent on an annualized basis. Excluding food and energy, Core PCE, increased 2.7 percent from one year ago. PCE release

45. June 27th and 30th – Tariff and trade negotiations between Canada and the U.S. continued

On Friday Trump suspended all trade and tariff negotiations with Canada in retaliation to Canada’s Digital Services Tax, which was cancelled on Monday, restarting trade talks.

46. July 3rd – Trade balances narrowed and widened

StatsCan reported that Canada’s merchandise trade deficit with the world narrowed from a record $7.6 Billion in April to $5.9 Billion in May. Exports to the U.S. (-0.9%) were down for a fourth consecutive month. Exports to countries other than the United States rose 5.7% in May to reach a record high of $47.6 Billion, the third consecutive monthly high. CBC and trade

The U.S. trade balance increased more than 18% to $71.5 Billion in May (up from $60.3 Billion in April) as exports fell according to the Bureau of Economic Analysis release. Imports also fell, but by a smaller percentage than exports. In May, the largest trade deficits in billions were with Mexico ($17.1), Vietnam ($14.9) and China ($14.0). Reuters and trade balance

47. July 3rd – U.S. job growth in June hit the average

The U.S. Bureau of Labor Statistics reported that total nonfarm payroll employment increased by 147,000 in June, higher than expectations and just below the 12-month average of 146,000. BLS release CNBC and jobs data

48. July 8th – “Big Beautiful Bill” moved markets lower as debt grows higher

Some of the downturn can be attributed to the approval and signing into law Trump’s “big, beautiful budget bill”. Projections from the Congressional Budget Office have deficits increasing by $3.3 Trillion over the next decade.

49. July 10th – Trade war continued with new letters from the American president

Tariff letters were sent by President Trump to major trading partners. “The resulting uncertainty is preventing companies an countries from making plans as the rule so global commerce give way to a state of chaos” according to a NY Times article. Canada and the U.S. had been negotiating toward an agreement before a deadline on July 21st until Trump sent a letter with a 35 percent tariff and a new deadline of August 1st.

50. July 11th – Canadian jobs growth surprised analysts

StatsCan released employment data for June. Expectations were for little change, however the Canadian economy surprised analysts by adding 83,000 jobs and unemployment fell 0.1% to 6.9%. This was the first increase in employment since January. The unemployment rate had increased for three consecutive months before the decrease in June. StatsCan release CBC and jobs

51. July 15th – Inflation data from Canada and the U.S.

Canada’s Consumer Price Index (CPI) rose 1.9% on a year-over-year basis in June, up from a 1.7% increase in May. On a monthly basis, prices rose 0.1% in June. StatsCan release CTV and CPI

The Bureau of Labor Statistics (BLS) reported that consumer price increases have accelerated in response to President Trump’s trade war and tariffs. In June, prices have risen 2.7% on a year-over-year basis, the same measure in May was 2.4%. Over the course of the month of June, prices rose 0.3%, a significant increase from May’s monthly inflation of 0.1%. BLS CPI release CNBC and CPI NYTimes and CPI

52. July 22nd – Magnificent Seven performance moves indexes higher

The TSX, S&P 500 and NASDAQ reached new all-time highs, and the Dow sat just 0.2% or just 112 points below its closing record of 45,014 reached back in December. The TSX and S&P 500 have risen seven and nine percent, respectively, since mid-June. Some instability may present itself this week as large trade deadlines loom, interest rate announcements await and corporate earnings from the Magnificent Seven arrive. Factset's analysis.

53. July 30th – Bank of Canada and Federal Reserve held rates steady

The Bank of Canada held its policy interest rate unchanged on Wednesday morning. It was the third consecutive interest rate decision that held rates firm at 2.75%. The Canadian economy has shown resilience despite the threats of American tariffs. Inflation has not responded as favourably. Since it appears that the U.S. president will not return to more open trade conditions, and will impose tariffs and other restrictions, the Bank of Canada has not, yet, taken steps to stimulate the economy. The Bank made projections based three scenarios: tariffs in-place as of July 27th, an escalation in tariffs, and a de-escalation in tariffs. CBC and interest rates BoC release

The Federal Reserve held their federal funds rate unchanged at a range of 4¼ to 4½ percent. The announcement included, “…recent indicators suggest that growth of economic activity moderated in the first half of the year. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated.” All but two of the Governors voted in-favour of maintaining rates at the current level. Fed release

54. July 31st – Canadian employment and economic growth move in different directions

On Thursday, StatsCan released jobs data for May showing that “payroll employment” increased by 15,300 in May, a slight increase from April’s 14,600. Over the past year payroll employment has increased 43,300 as of May. StatsCan and payroll employment

Canadian Gross Domestic Product edged downward by 0.1% in May, the second consecutive month of decline. Goods producing industries like mining, quarrying and oil and gas extraction, while manufacturing expanded. Services sectors were unchanged overall. StatsCan and GDP

55. August 1st – Trump’s tariffs arrived

To begin the month, 35% tariffs were imposed on Canadian imports to the U.S. as negotiations continue. Talks or communication was not on-going at the highest level between Prime Minister Carney and President Trump when the tariffs came into force. Prime Minister Carney has indicated that negotiations with the U.S. president will resume when appropriate. CBC and Tariffs

The month began with a disappointing Employment Situation Summary that caused President Trump to fire the chief statistician at the Bureau of Labor Statistics. Trump has been calling for an interest rate reduction, and the economy’s poor job performance could trigger a rate drop.

56. August 5th – trade deficits affected by threatened and enacted tariffs

Canada’s trade deficit continued to widen and reached its second highest monthly level at $5.9 Billion. Imports grew faster than exports as inbound shipments of high value oil equipment arrived in June. Exports to the U.S. have fallen to 70% of total exports, compared with 83% in June 2024. Reuters and Can trade balance

The Bureau of Economic Analysis announced that June’s U.S. trade deficit shrank 16% to $60.2 Billion as exports eased 0.5% (-$1.3 Billion) and imports fell 3.7% (-12.8 Billion) compared to May. The trade deficit reached its lowest level in two years as the trade gap with China and imports of consumer goods dropped sharply. BEA release Reuters and US trade balance

57. August 7th – China’s exports surged to skirt U.S. tariffs

China’s exports increased more than expected in July. Shipments sent to other countries that often forward Chinese goods on to the U.S. jumped. Shipments directly to the U.S. fell more than 20%. Overall, China’s exports grew by 7.2% compared with July 2024. NYT and China's trade

58. August 8th – Canadian employment fell dramatically, U.S. CPI rose

Canadian employment declined by 41,000 jobs in July according to StatsCan’s Labour Force Survey after an increase of 83,000 in June. The employment rate fell 0.2% to 60.7% and the unemployment rate was unchanged at 6.9%. Analysts expected employment to increase by 13,500 and unemployment to tick up to 7.0%. The employment decline was concentrated among youth aged 15 to 24 (-34,000). The industries that lost the most jobs was information, culture and recreation (-29,000) and construction (-22,000). CBC and Labour Force Survey

59. August 11th – China’s tariffs given 90-day reprieve

President Trump signed a 90-day extension delaying the introduction of 145% tariffs on Chinese imports, and China delayed its retaliatory tariffs of 125% on U.S. imports. The existing tariffs on imports from and exports to China are 30% and 10%, respectively. CNBC and China tariffs

60. August 12th – U.S. inflation may not delay Fed rate cuts

The CPI increased 0.2% for the month and 2.7% on a year-over-year basis. Core CPI, which excludes more volatile food and energy price changes, increased 0.3% for the month and 3.1% compared to last year. Core inflation rose more rapidly in July than it has in the past five months. With delays and renegotiations, July prices do not yet reflect all the effects of threatened and implemented tariff, suggesting that inflation could continue to increase in the coming months. CNBC and CPI BLS CPI release NYTimes and CPI

Many analysts believe the weakness in the employment situation will encourage the Federal Reserve to cut interest rates despite rising inflation in July. On the morning of the CPI announcement CME's FedWatch tool listed the probability of a rate cut on September 17th at 94%.

61. August 14th – Producer inflation soared

The Bureau of Labor Statistics released the Producer Price Index (PPI) showing that wholesale prices jumped 0.9% in July, after holding steady in June and rising 0.4% in May. The year-over-year rate of producer inflation grew to 3.3% for July, the highest rate in 5 months when February’s PPI was 3.4%. BLS PPI release

62. August 15th - Trump and Putin met in Alaska

U.S. President Donald Trump met with Russian leader Vladimir Putin in Alaska to discuss his war with Ukraine. President of Ukraine, Volodymyr Zelenskyy, was not invited to the summit meeting, whose exclusion drew the ire of NATO and the European Union leaders. The progress, if any, achieved from the summit has not materialized in a meaningful manner, yet. CBC and Alaska Summit

63. August 28th – U.S. Gross Domestic Product revised upward

During the period of April through June the U.S. economy grew by 3.3%, better than the 3.0 estimated initially. Imports subtract from GDP total in the calculation, and after stockpiling before tariffs were introduced, imports in the latter stages of the quarter fell by nearly 30%, which propped up GDP numbers. CNBC and GDP

64. August 29th – Canadian economy shrank

StatsCan reported that Gross Domestic Product declined by 0.4% in the second quarter after rising 0.5% in the first quarter. The decline was driven by substantial reductions in exports (down 7.5% in Q2) and business investments in machinery and equipment. U.S. initiated tariffs and Canada’s response, and the underlying uncertainty caused by the trade conflict, created the environment for an economic slowdown. StatsCan release

65. August 29th – PCE inflation remained above goal, tariffs deemed illegal, and rates could fall

The Federal Reserve’s preferred inflation indicator, the Personal Consumption Expenditures (PCE) price index rose 2.6% over the past year, and core inflation that excludes food and gasoline rose 2.9%. Both are above the Fed’s goal of 2% showing tariffs imposed by Donald Trump have raised prices. Inflation has returned to February’s level, which had been falling until tariffs were announced. BEA PCE release CNBC and PCE

A federal appeals courts has declared that Trump’s tariffs are illegal after upholding a May ruling by the Court of International Trade. The tariffs will remain in-place temporarily to allow a further appeal to the U.S. Supreme Court. BBC and tariff ruling

Also, despite the mixed economic news CME's FedWatch tool has increased the likelihood of a cut to the federal funds rate by the Federal Reserve on September 17th.

66. September 5th – Canadian and U.S. employment reported disappointing results

Canada’s Labour Force Survey showed that employment dropped by 66,000 in August after falling 41,000 in July. The employment decline in August was mostly part-time work (-60,000), and full-time employment was stable following a decline in July (-51,000). StatsCan LFS release

“Total nonfarm payroll employment changed little in August (+22,000) and has shown little change since April” according to the U.S. Bureau of Labor Statistics’ Employment Situation Summary (ESS) release for August. During the first five months of 2025 U.S. employment grew by an average 168,000 per month, which included 228,000 in March, which was prior to the announcement of tariffs on April 2nd. BLS ESS archive

67. September 5th – Prime Minister Carney announced economic recovery plan

Prime Minister Carney announced actions to strengthen the Canadian economy, reduce reliance on the U.S., and promote trade on a broader scale. CBC and Carney's plan

68. September 11th – U.S. CPI remained above goal

The Consumer Price Index (CPI) crept upward in August. The year-over-year consumer inflation rate was 2.9%, and the month-to-month increase was 0.4%. A month earlier in July, the annual rate was 2.7%. Core CPI, which excludes more volatile food and energy, climbed at an annual rate of 3.1%, and 0.3% for the month. BEA CPI 250911 CNBC and CPI

69. September 16th – Canadian CPI edged up in August, remained at goal

According to the StatsCan release, the year-over-year Consumer Price Index (CPI) increased 1.9% in August, up from a 1.7% increase in July. The CPI decreased 0.1% over the month of August. StatsCan CPI release CBC and CPI

70. September 17th – Bank of Canada and Federal Reserve lowered policy interest rates

Inflation at current levels does not pose a risk, and with economic growth and employment waning, the Bank of Canada lowered its policy interest rate on Wednesday morning. The interest rate charged between financial institutions and the Bank, the overnight rate, was lowered by ¼ percent (25 basis points). Bank had last adjusted rates on March 12, 2025. The Bank’s statement indicated that “Canada’s GDP declined by about 1½% in the second quarter, as expected, with tariffs and trade uncertainty weighing heavily on economic activity.” Bank of Canada release CBC and interest rates

The U.S. Federal Reserve took similar action to lower the federal funds rate to a range of 4 to 4¼ percent. The Fed’s statement began, “Recent indicators suggest that growth of economic activity moderated in the first half of the year. Job gains have slowed, and the unemployment rate has edged up but remains low. Inflation has moved up and remains somewhat elevated.” Federal Reserve release CNBC and Fed rates

71. September 26th – U.S. PCE confirmed inflation above goal rate

The Bureau of Economic Activity (BEA) reported that the Personal Consumption Expenditures price index (PCE), the Federal Reserve’s preferred inflation indicator, rose in August at 2.7% on a year-over-year basis. In July, prices rose 2.6%. The slight uptick in consumer inflation is unlikely to change the course of Federal Reserve interest rate policy. On September 17th, the Fed indicated that two additional rate cuts were possible in 2025. BEA PCE release CNBC and PCE

72. September 26th – GDP rebounded in Canada and the U.S.

Gross Domestic Product (GDP) has been more resilient than expected in both the U.S. and Canada according to the latest announcements. Canada’s GDP grew 0.2% in July, the first increase in four months.

U.S. GDP grew at an annual rate of 3.8% in the second quarter according to the BEA’s “third estimate”. BEA GDP release StatsCan GDP release

73. September 30th – U.S. government shut down by budget battle

At midnight the U.S. federal government did not have funds to operate as the latest budget bill ended without a replacement. Despite the turmoil the S&P 500 reached a new record as equity markets believe the shutdown will be short-lived. CNBC live updates

74. October 1st – U.S. government shut-down began

A government shutdown began after the U.S. Congress was unable to reach an agreement to extend funding to avoid the disruption of services and benefits. One of the casualties of the budget impasse was the scheduled Nonfarm Payroll Report from the Bureau of Labor Statistics. The payroll report is considered “the King of the Numbers” and is closely watched, along with interest rates and inflation, to inform traders. Reuters and shutdown

75. October 1st – Bank of Canada released its logic on mid-September interest rate cut

The Bank of Canada released its Summary of Deliberations from its September 17th ¼ point interest rate cut. Since the July Monetary Policy Report, “the global economy had proven resilient to increased US tariffs in the first half of the year, there were increasing signs that economic growth was slowing.” BoC SoD

76. October 7th – Canada’s trade balance affected by U.S. tariffs

Prime Minister Carney and President Trump met in Washington to discuss several issues, including trade between the two countries as Canada’s trade surplus with the U.S. fell from $7.4 billion in July to $6.4 billion in August. CBC and trade

77. October 10th – Canada’s employment numbers rebounded

StatsCan released the latest employment report. Employment increased by 60,000 in September, after declining by more than a combined 100,000 in July and August. The unemployment rate was unchanged by 7.1%. The turnaround from job losses to growth and an increase above analyst expectations is a positive sign for the health of the Canadian economy despite the on-going trade war and negotiations with the U.S. StatsCan employment report CPI and employment

78. October 16th – Market volatility peaked mid-month

The primary measure of volatility is the CBOE VIX Volatility Index. At the highest level since President Trump's Liberation Day, the VIX peaked at 25.31, one week earlier it was 16.43. The calculation of VIX is complicated, however the 54% increase in one week indicates how quickly and dramatically volatility rose based on Trump’s trade war and the government shutdown. To better understand VIX, values below 20 represent stability, and values over 30 indicate greater market fear and uncertainty.

79. October 21st – Canada’s consumer inflation moved up by one-half percent

StatsCan announced that the Consumer Price Index (CPI) rose 2.4% on a year-over-year basis in September, up from a 1.9% increase in August. Economists had expected a rise of 2.2%. A slower decline in prices for gasoline and a larger increase in grocery prices conspired together to push the inflation rate higher. The Bank of Canada preferred inflation indicator set is Core CPI, which excludes food and energy. The three measures of Core CPI in September were 2.7%, 3.2% and 3.1%, with 3% as the goal. StatsCan CPI release CBC and CPI

80. October 23rd – Trump ended tariff negotiations with Canada, again

President Trump ended tariff negotiations on Thursday night in reaction to a campaign that includes a video advertisement that the Government of Ontario has been airing in the U.S. Trump has attributed the ad to Canada, not Ontario, which may have contributed to his decision to cease trade talks.

81. October 24th – U.S. consumer inflation moved upward

Despite the U.S. government shutdown the Bureau of Labor Statistics released CPI data for September. On a seasonally adjusted consumer prices rose 0.3 percent, slightly below the 0.4 percent measured in August. On a year-over-year basis the all-items index rose 3.0 percent versus 2.9 percent in August. BLS CPI release CNBC and CPI

82. October 29th – Bank of Canada and Federal Reserve cut rates

For the second consecutive announcement the Bank of Canada cut its overnight rate, which now sits at 2¼ percent. At the press conference, Governor Tiff Macklem concluded, “With ongoing weakness in the economy and inflation expected to remain close to the 2% target, Governing Council decided to cut the policy rate by 25 basis points.” BoC release CBC and BoC

The U.S. Federal Reserve stated “Inflation has moved up since earlier in the year and remains somewhat elevated” as the government shutdown severely limited the dissemination of economic data. Nonetheless the Fed lowered the federal funds rate by ¼ percent to a range of 3¾ to 4 percent. Fed release CNBC and Fed

83. October 30th – European Central Banks held rates unchanged

The European Central Bank decided to maintain its interest rates since their consumer inflation has settled around their 2% goal and employment has stabilized. The effects of the trade war on European economies are more muted than on North American economies. ECB summary ECB release

84. November 4th – Federal Liberals tabled their budget in the House of Commons

Prime Minister Mark Carney introduced the first Canadian federal budget in 18 months. The promised 25% reduction in minimum RRIF withdrawals was not included. Bare trust reporting will finally begin in 2027 for year-ends of December 31, 2026, and later.

85. November 7th – Canadian employment bounced-back

The Labour Force Survey from StatsCan reported that employment increased by 67,000 in October and the unemployment rate declined by 0.2% to 6.9%. Wages have increased 3.5% (+ $1.27 to $37.06) on a year-over-year basis in October, following growth of 3.3% in September. StatsCan release

86. November 12th – Government shutdown ended

The longest government shutdown in U.S. history finally ended, and the reopening will take several weeks, if not months, to achieve.

87. November 14th – Effects of shutdown reduced likelihood of Fed rate cut

Unfortunately, the positive effect of reopening was tempered for investors. During the shutdown the Bureau of Labor Statistics missed reporting several key economic indicators, and it appears that several may never be reported. Missed reports in 2025 will prevent the interpretation of annualized trends in 2026 when year-over-year comparisons are impossible. Doubt has begun to rise whether the Federal Reserve has sufficient evidence to reduce interest rates. As of November 14th CME's FedWatch tool indicated that the likelihood of a ¼ point rate cut was slightly less than rates remaining unchanged. NYTimes, data and rate cuts CNBC and data

88. November 17th – Canadian consumer inflation edged upward

StatsCan reported that the Consumer Price Index (CPI) rose 2.2% on a year-over-year basis in October, slightly lower than the 2.4% increase in September. CPI fell due to lower gasoline prices and a slowing of price increases for groceries. StatsCan CPI release

Canadian budget bill passes House vote

The House of Commons approved the 2025 budget bill, which was enabled by four abstentions and the support of Green Party MP, Elizabeth May, the vote passed 170-168. Watch highlights here

89. November 20th – U.S. jobs added and finally returned to April levels

The U.S. Employment Situation Summary revealed that “total nonfarm payroll employment edged up by 119,000 in September but has seen little change since April. The unemployment rate changed little in September at 4.4 percent. BEA current release

90. November 21st – Fed released its meeting minutes and rate cuts have become less certain

The U.S. Federal Reserve released the minutes from its interest rate meeting of October 28-29 when the federal funds rate was reduced by ¼ percent. Some committee members stated that lowering the rate could entrench inflation above the 2% goal and signal a reduced commitment to achieving price stability. Reuters and Fed minutes

91. November 25th – More economic releases cancelled by U.S. administration

Three import indicators, jobs, inflation and GDP, have been delayed or cancelled with the now-ended government shutdown as the excuse for withholding data. The tariff scheme and mass deportations has reduced U.S. GDP by 7 percent according to one source, and consensus is growing that bad news is being withheld. MSN Yahoo

92. November 28th – Canadian GDP rebounds in Q3

“Real gross domestic product (GDP) rose 0.6% in the third quarter of 2025, after falling 0.5% in the second quarter” according to the StatsCan release on November 28th. The annualized GDP growth rate in the quarter was 2.6%. CBC and GDP

93. December 5th – Canadian employment rose

Canadian “employment increased by 54,000 in November, driven by gains in part-time work” according to StatsCan's Labour Force Survey. The unemployment rate fell 0.4 percentage points to 6.5%. Although total employment was stagnant from January to August, employment has increased 181,000 over the last three months (September, October and November).

94. ADP reported 8th – ADP reported job losses

The U.S. Bureau of Labor Statistics jobs report has been delayed more than two weeks until December 16th, which is after the next Fed interest rate decision. Payroll processor, ADP, reported that private employers in the U.S. shed 32,000 jobs in November. Small businesses, which are sensitive to economic influences and sentiment, led the drop in employment. ADP employment report

95. December 5th – Canadian employment continued three month rise

Canadian “employment increased by 54,000 in November, driven by gains in part-time work” according to StatsCan's Labour Force Survey. The unemployment rate fell 0.4 percentage points to 6.5%. Although total employment was stagnant from January to August, employment has increased 181,000 over the last three months (September, October and November).

The Federal Reserve’s preferred inflation indicator, the Personal Consumption Expenditures price index, (PCE) was released. Both the overall PCE and Core PCE (excluding food and energy) increased 2.8 percent in September. Nearly all of the increase in current-dollar personal consumption expenditures, $63 Billion of $65.1 Billion, reflected an increase in spending for services. PCE release for September

Both the Bank of Canada and Federal Reserve have mandates to control inflation and maximize employment. The Canadian Consumer Price Index sits is 2.2% on a year-over-year basis at the end of October, and the recent job gains suggest the Bank of Canada may hold rates steady. The lack of official employment data and slightly stale, yet better than expected inflation numbers have a Federal Reserve rate cut predicted as almost 90 certain. CNBC, PCE and Fed CBC and rates

96. ADP reported 8th – ADP reported job losses

The Bank of Canada kept the overnight rate at 2.25%. Controlling consumer inflation, one of the Bank’s major objectives, was achieved at 2.2% in October. The Bank’s rationale also included the Consumer Price Index (CPI) remained close to the 2% target, Canadian Gross Domestic Product that grew at an annualized rate of 2.6% in the third quarter, Canada’s labor market is improving with solid job gains in the last three months and a decline to the unemployment rate. BoC release

97. December 15th – Canadian consumer prices rose 2.2%

The Canadian Consumer Price Index (CPI) rose 2.2% on a year-over-year basis in November, matching October’s result. Month-over-month in November, the CPI rose 0.1%. Prices for services rose more slowly, and grocery price inflation was the highest since the end of 2023, driven by beef and coffee prices that have risen 17.7% and 27.8%, respectively, in the last year. StatsCan release CBC and CPI

98. December 16th – U.S. employment changed little

The BLS also reported the November's Employment Situation Summary stating “total nonfarm payroll employment changed little in November (+64,000) and has shown little net change since April.” The unemployment rate was 4.6% and was little changed from September. Again, no data was collected in October due to the federal government shutdown. Since November 2024 the number of unemployed persons has risen almost 10% to 7.8 million, and the number of people who want a job has risen over 1 million to 6.1 million over the same period. The Fed may increase its focus in this area.

99. December 18th – U.S. consumer inflation rose slightly

The Consumer Price Index in the United States increased 2.7% on a year-over-year basis. Over the t wo months from September to November 2025 the CPI rose 0.2%. The Bureau of Labor Statistics (BLS) did not collect or publish CPI inflation data for October 2025 “due to a lapse in appropriations.” Analysts are suggesting that a “tame inflation” rate could focus the Federal Reserve on maximizing employment. Although, the likelihood of a January rate-cut remained low, the possibility for a March cut is rising according to CME's FedWatch tool. BLS release CNBC and CPI

The European Central Bank kept its three key lending rates unchanged on Thursday. Its updated assessment confirmed that inflation should stabilize at the 2% target in the medium term. ECB release

Ryan Gubic is the founder of MRG Wealth Management Inc. operating as MRG Wealth (“MRG”) and is a Portfolio Manager with MRG investments of Aligned Capital Partners Inc. (“ACPI”). The opinions expressed are not necessarily those of MRG, ACPI, or Ryan Gubic. This material is provided for general information and the opinions expressed and information provided herein are subject to change without notice. Every effort has been made to compile this material from reliable sources however no warranty can be made as to its accuracy or completeness. Before acting on the information presented, seek professional financial advice based on your personal circumstances. ACPI is a full-service investment dealer and a member of the Canadian Investor Protection Fund (“CIPF”) and the Canadian Investment Regulatory Organization (“CIRO”). Investment services are provided through MRG Investments, an approved trade name of ACPI. Only investment-related products and services are offered through MRG Investments of ACPI and covered by the CIPF. Financial planning and insurance services are provided through MRG. MRG is an independent company separate and distinct from MRG Investments of ACPI.

Dollars and Sense

Discover more

Dive into some advice directly from our Founder and Personal CFO.

What Happened in the Markets in June 2026